Net worth basics – Calculating, tracking and growing

They say ‘What doesn’t get measured, doesn’t get done’ and they couldn’t be more right. Your net worth is like the vital sign of your financial being.

I want to start however by saying that your net worth is very different from your self worth. You, as a person, are a lot more than the money you have and it is important to remember that. Your financial being is important, however, your social being is indispensable.

Now that we’ve established that, let us talk about how to calculate your net worth. Your net worth is simply the value of everything you own, minus, the value of everything you owe. In essence, your Assets minus your Liabilities.

Net Worth = Assets – Liabilities (Debt)

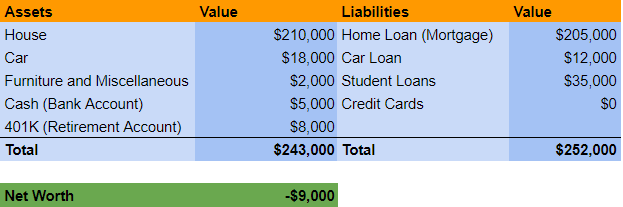

For Example, consider the below sample financial situation of one Jane Doe,

Jane’s net worth would be the difference between Assets and Liabilities which is equal to negative $9,000.

You can see then how in order to increase their net worth, they’d want to increase the left hand side while decreasing the right hand side. If items on the left were things that increase in value on their own, they automatically add to the net worth. The house and 401K are in this category. Hence, you can classify them as ‘Investments’. The car, furniture, clothes are all guaranteed depreciating assets. They are worth less today than they were yesterday. Hence, they are not investments. They are necessities however. You need a car to get around. You need clothes and furniture. But you also control how much to spend on these things. The less you spend on these depreciating things, the more dollars you can ‘Invest’ toward growth assets adding to your net worth over time.

If Jane sticks to her situation, in 5 years, below would be her situation.

The ultimate goal should be to make the right side of the above table to be zero as quickly as you can. Imagine Jane trades in the $18,000 car that she still owes $12,000 on, and was paying $380 a month on and bought a 10 year old $6000 car. The situation changes to below The net worth doesn’t change but starting next month, Jane starts saving $380 every subsequent month to pay towards her student loan instead.

Doesn’t make a massive difference in the moment but in 5 years, with diverting the car payment towards her student loan, below would be the situation.

You can see that a simple decision would have helped add $22,000 to your net worth in 5 years. Now that Jane is almost done paying off her student loans and car loan. if she continues to drive the same car and invests both her car payment and student loan payments in the stock market, by year 10, below would be her situation.

A simple decision then compounded over 10 years added almost $90,000 to her net worth over 10 years. The cost? Downgrade and control your lifestyle. The kicker? Jane Doe was me in 2012. I traded in a 2008 Subaru Impreza WRX for a 2002 Honda Civic. The rest, as they say, is history.

For more strategies, consider subscribing to the blog.